The Slow Roll of Monetary Policy – 10/14/2024 Update

“The Slow Roll of Monetary Policy,” was featured in our quarterly letter “The Long & Short of It” for five quarters from January 2023 to April 2024. Here, we will continue to show the slow, steady progression of monetary policy’s lag as it works through the economy and drives inflation. (See prior publications in previous quarterly letters.)

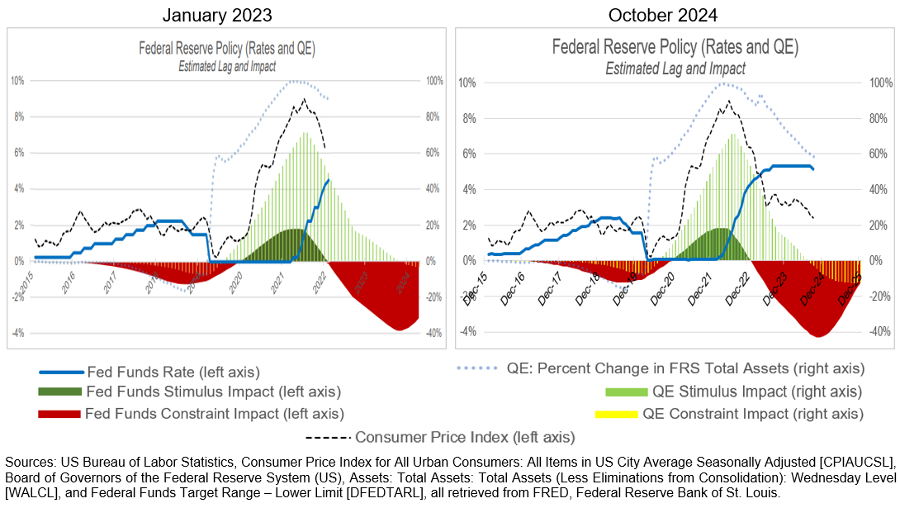

September 2024 Consumer Price Index (CPI) rose by 0.18%, which annualizes to 2.2%. The actual increase for the 12 months was 2.4% (see chart to right above), though the most recent six months rose at an annualized rate of 1.6%. Core CPI, which excludes food and energy, moderates less willingly. It rose 0.31% for the month, which annualizes to 3.7%. The actual increase for the year was 3.3%, though the six months rose at an annualized rate of 2.6%. Despite the slight uptick for the month, the overall trend of inflation is one of moderation toward the Fed’s targeted goal of 2% (left axis). Expansive fiscal deficits continue to fight the Fed’s policy, but as long as inflation looks to be moving toward the Fed’s target, stock markets are likely to remain happy. If that target is reached and inflation is reported to be “Just right,” it will be difficult to produce further improvement and stock market volatility may return. We look for the Fed to eventually overshoot and see inflation on the lower side of target.

September 2024 Consumer Price Index (CPI) rose by 0.18%, which annualizes to 2.2%. The actual increase for the 12 months was 2.4% (see chart to right above), though the most recent six months rose at an annualized rate of 1.6%. Core CPI, which excludes food and energy, moderates less willingly. It rose 0.31% for the month, which annualizes to 3.7%. The actual increase for the year was 3.3%, though the six months rose at an annualized rate of 2.6%. Despite the slight uptick for the month, the overall trend of inflation is one of moderation toward the Fed’s targeted goal of 2% (left axis). Expansive fiscal deficits continue to fight the Fed’s policy, but as long as inflation looks to be moving toward the Fed’s target, stock markets are likely to remain happy. If that target is reached and inflation is reported to be “Just right,” it will be difficult to produce further improvement and stock market volatility may return. We look for the Fed to eventually overshoot and see inflation on the lower side of target.

Amy Abbey Robinson, CIMA® RMA® amy@robinsonvalue.com

Charles W. Robinson III, CFA® charles@robinsonvalue.com